If you are comparing a solar loan vs lease, the biggest question is not only which option has the lower monthly payment.

The better question is:

Which option gives you the best combination of ownership, savings, flexibility, risk, and long-term ROI?

A solar loan usually means you finance the system and own it while making payments. A solar lease usually means a solar company owns the system and you pay a monthly amount to use the system or benefit from the electricity it produces.

Both can reduce upfront cost compared with paying cash. But they are very different when it comes to incentives, resale, maintenance, contract terms, payback period, and long-term return.

This guide explains the practical differences between a solar loan and a solar lease so homeowners can compare quotes more carefully before signing a contract.

Before choosing a financing option, use the MySolarROI solar ROI calculator to estimate how system cost, financing terms, electricity savings, incentives, and payback period may affect your long-term ROI.

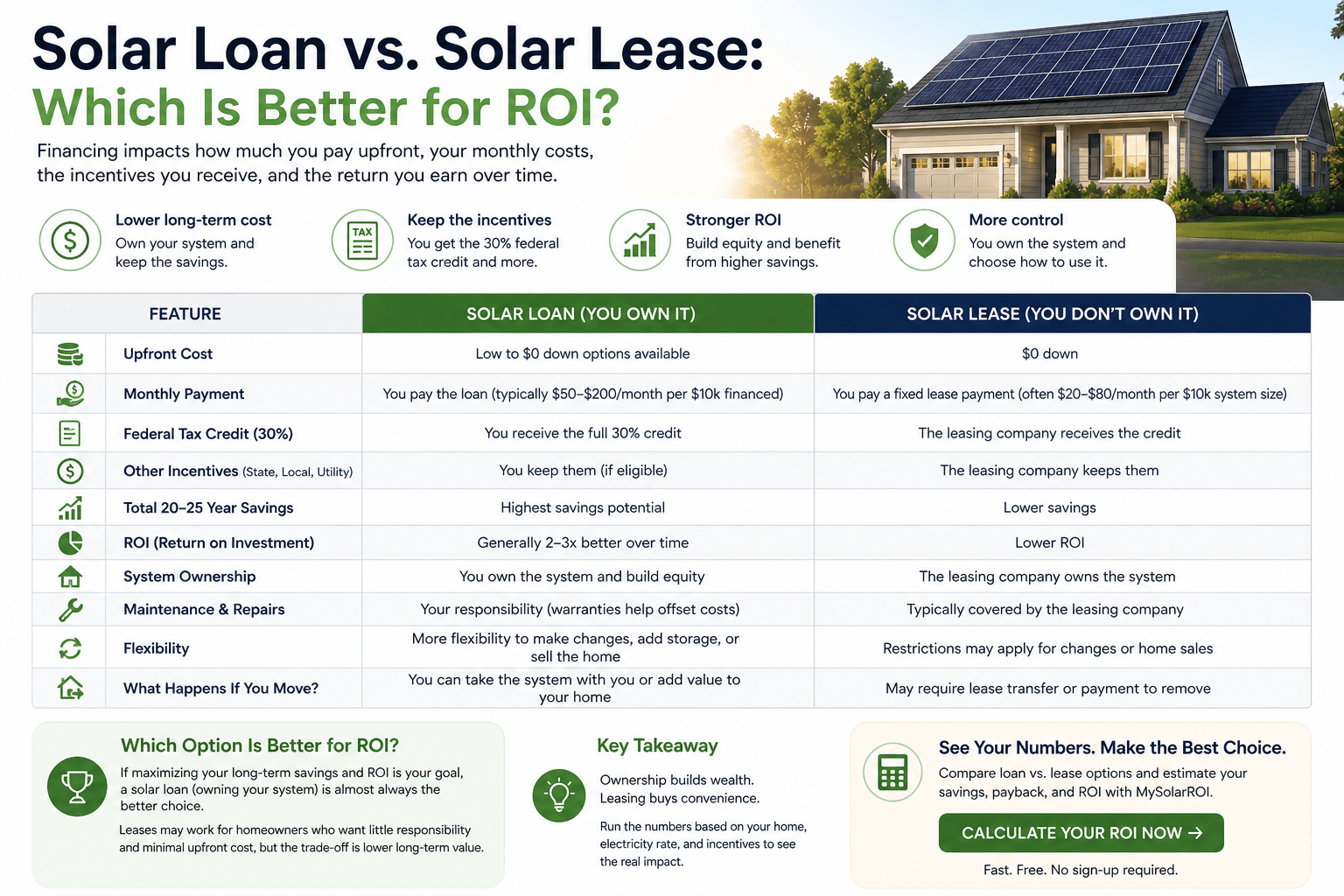

Solar Loan vs Lease: Quick Comparison

The simplest difference is ownership.

With a solar loan, you usually own the solar system. With a solar lease, the solar company or financing company usually owns the system.

| Factor | Solar Loan | Solar Lease |

|---|---|---|

| Who usually owns the system? | Homeowner | Solar company or financing company |

| Upfront cost | Often low to moderate | Often low |

| Monthly payment | Loan payment | Lease payment |

| Long-term savings potential | Can be stronger if loan terms are fair | Usually lower than ownership |

| Incentive access | Homeowner may qualify if eligible | System owner may receive incentives |

| Maintenance responsibility | Homeowner, installer, and warranties | Often handled by system owner, depending on contract |

| Home sale complexity | Loan payoff or transfer may matter | Lease transfer or buyout may matter |

| Best fit | Homeowners who want ownership without paying all cash upfront | Homeowners who want lower upfront cost and less ownership responsibility |

In many ROI-focused cases, a transparent solar loan can create stronger long-term upside than a lease because the homeowner owns the system. But loan terms matter. A high-fee or high-interest solar loan can reduce savings significantly.

A lease may be easier upfront, but it can limit ownership benefits, incentive access, and resale flexibility.

What Is a Solar Loan?

A solar loan is a financing option that lets you pay for a solar panel system over time.

In most cases, the homeowner owns the solar system, but also has a loan obligation. The loan may be offered through the installer, a solar lender, a bank, a credit union, or another financing company.

Solar loans can be secured or unsecured, and the terms can vary widely.

Solar loan benefits

- You usually own the system.

- You may be able to install solar with little or no upfront cash.

- You may keep access to ownership-based incentives if you qualify.

- After the loan is paid off, the system may continue producing savings.

- Home sale may be simpler than with a lease if the loan is paid off.

- You may have more control over equipment and installer choices.

Solar loan drawbacks

- Interest and fees can reduce ROI.

- The financed price may be higher than the cash price.

- Dealer fees may be built into the system price.

- Long loan terms can hide the real cost.

- You are usually responsible for ownership-related issues.

- The loan may need to be paid off or handled when selling the home.

A solar loan can be a good option when the system price is fair, the interest rate is reasonable, fees are transparent, and the homeowner plans to stay long enough to benefit from the system.

For a broader financing comparison, read the solar financing comparison guide.

What Is a Solar Lease?

A solar lease is an agreement where a solar company usually installs and owns the solar system on your home. You pay a monthly lease payment for the right to use the system or benefit from the electricity it produces.

Because you usually do not own the system, a lease is different from a loan.

Solar lease benefits

- Often little or no upfront cost.

- May include monitoring and maintenance.

- May reduce electricity costs if lease payments are lower than bill savings.

- Can appeal to homeowners who do not want to own solar equipment.

- System owner may handle repairs depending on contract terms.

Solar lease drawbacks

- You usually do not own the system.

- The solar company may receive incentives, not you.

- Monthly lease payments may increase if there is an escalator.

- Long-term savings are often lower than with ownership.

- Contract transfer can complicate selling the home.

- Buyout or removal options may be limited or expensive.

- You may have less flexibility to modify the system.

A solar lease may be practical for some homeowners, but it should be reviewed carefully. Do not judge a lease only by the first-year payment.

Solar Loan vs Lease for ROI

Solar ROI depends on what you invest and what you receive in return.

A solar loan can often produce stronger ROI than a lease because you usually own the system and may benefit from more of the long-term savings after the loan is paid off.

A lease may provide lower upfront cost and less maintenance responsibility, but much of the financial upside may stay with the system owner.

| ROI Factor | Solar Loan | Solar Lease |

|---|---|---|

| Ownership upside | Homeowner may benefit from long-term system value | System owner usually retains ownership value |

| Incentives | Homeowner may qualify if eligible | System owner may receive incentives |

| After payment period | Potential for lower bills after loan payoff | Lease payments continue during contract term |

| ROI calculation | Can be based on net system cost, financing cost, and savings | Often based on lease payment vs utility bill savings |

| Long-term upside | Can be higher with fair loan terms | Usually more limited |

However, a bad loan can be worse than a reasonable lease. If the loan includes high dealer fees, high interest, or a long repayment term, the ownership advantage may be reduced.

For ROI math, read the how to calculate solar ROI guide.

Solar Loan vs Lease for Monthly Cost

Monthly payment is important, but it is not the full story.

A solar loan payment may be higher than a lease payment, especially if the loan term is shorter. But the homeowner may own the system and eventually finish paying the loan.

A lease payment may be lower at first, but the contract may last 20 years or more and may include annual increases.

| Monthly Cost Question | Why It Matters |

|---|---|

| What is the first-year monthly payment? | Shows short-term affordability |

| Does the payment increase? | Escalators can reduce future savings |

| What is the total contract cost? | Shows long-term cost, not just monthly payment |

| What is the loan APR? | Interest affects real system cost |

| Are there dealer fees? | Fees may be hidden in the financed price |

| What happens after the loan is paid? | Ownership may create more long-term upside |

Do not choose the lowest monthly payment without checking the total cost and contract terms.

Solar Loan vs Lease for Incentives

Incentive treatment is one of the biggest differences between loans and leases.

With a solar loan, the homeowner usually owns the system. That may allow the homeowner to claim certain ownership-based incentives if they qualify.

With a solar lease, the solar company or financing company usually owns the system. That may mean the system owner receives available incentives, not the homeowner.

| Incentive Question | Solar Loan | Solar Lease |

|---|---|---|

| Who owns the system? | Usually homeowner | Usually solar company or financing company |

| Who may receive ownership-based incentives? | Homeowner may qualify | System owner may qualify |

| Are incentives reflected in pricing? | May reduce homeowner’s net cost if eligible | May be reflected in lease payment, but ask clearly |

| Do tax rules matter? | Yes, if tax credits are involved | Yes, but homeowner may not be claimant |

In 2026, homeowners should be especially careful with federal residential tax credit assumptions. Do not assume the old 30% federal residential credit applies to new 2026 installations. Review the federal solar tax credit 2026 guide and verify current IRS rules before relying on any tax credit assumption.

You can also use the solar tax credit calculator guide to understand how incentive assumptions affect payback and ROI.

Solar Loan vs Lease for Maintenance

Maintenance responsibility is another key difference.

With a solar loan, you usually own the system. That means you rely on equipment warranties, workmanship warranties, installer support, and your own follow-up if something goes wrong.

With a lease, the system owner may handle monitoring, maintenance, and repairs, depending on the contract.

| Maintenance Issue | Solar Loan | Solar Lease |

|---|---|---|

| Monitoring | Homeowner or installer platform | Often system owner or lease provider |

| Equipment repairs | Warranty and installer support matter | Often handled by system owner, depending on terms |

| Inverter replacement | May be homeowner responsibility if outside warranty | May be covered by lease contract |

| Roof work coordination | Homeowner must coordinate removal/reinstall if needed | Contract terms control removal and reinstall process |

| System performance | Depends on warranty and installer agreement | May include performance terms, but read carefully |

A lease may reduce some maintenance responsibility, but the contract should clearly explain what is covered and what is not.

Solar Loan vs Lease When Selling Your Home

Home sale issues can be very different for loans and leases.

With a solar loan, you may need to pay off the loan, transfer it, or handle it at closing depending on the loan terms.

With a lease, the buyer may need to assume the lease, qualify for transfer, or negotiate a buyout.

| Home Sale Question | Solar Loan | Solar Lease |

|---|---|---|

| Can the system transfer easily? | Depends on loan terms and payoff | Depends on lease transfer rules |

| Does the buyer need approval? | Usually less common, but loan terms matter | Often possible if lease transfer is required |

| Can you buy out the agreement? | Usually loan payoff is possible | Buyout terms vary by contract |

| Could it complicate closing? | Possible if loan or filing must be handled | Possible if buyer resists or transfer is slow |

If you may sell your home before the contract ends, review this section carefully before choosing a lease or a long-term loan.

Ask for written answers about transfer, payoff, buyout, system removal, and buyer requirements.

Mini Case Study: Solar Loan vs Lease ROI Scenario

Here is a simplified homeowner example. These numbers are for illustration only and are not guaranteed.

Actual results depend on location, system cost, electricity rates, roof conditions, incentives, utility rules, financing terms, lease terms, maintenance, and how long the homeowner stays in the home.

| Assumption | Solar Loan Example | Solar Lease Example |

|---|---|---|

| System ownership | Homeowner | Solar company |

| Gross system value | $24,000 | Installed under lease contract |

| Monthly payment | Loan payment | Lease payment |

| Incentives | Homeowner may qualify if eligible | System owner may receive incentives |

| After payment period | Homeowner may keep system benefits after loan payoff | Lease terms continue until contract ends or buyout occurs |

| Maintenance | Warranty and homeowner follow-up | Often included, depending on contract |

| Home sale | Loan payoff or transfer may matter | Lease transfer or buyout may matter |

In this scenario, the loan may offer stronger long-term ROI if the system is fairly priced and the loan terms are reasonable.

The lease may feel simpler upfront, especially if maintenance is included, but the homeowner may give up ownership upside and direct incentive access.

The better choice depends on the actual numbers:

- cash price

- financed price

- APR

- dealer fees

- lease payment

- lease escalator

- contract length

- utility savings

- incentive treatment

- home sale plans

Run both options through the MySolarROI solar ROI calculator before deciding. Compare payback period, monthly cash flow, and long-term savings under conservative assumptions.

When a Solar Loan May Be Better

A solar loan may be better when:

- you want to own the system

- the cash price is fair

- the APR is reasonable

- dealer fees are low or transparent

- you plan to stay in the home long enough

- you may qualify for ownership-based incentives

- you want more long-term savings potential

- you are comfortable handling ownership responsibilities

A solar loan may be weaker when:

- the financed price is much higher than the cash price

- the loan term is very long

- interest and fees reduce most savings

- you may move soon

- the system is overpriced

- you do not want ownership responsibility

When a Solar Lease May Be Better

A solar lease may be better when:

- you want little or no upfront cost

- you do not want to own the system

- maintenance coverage is important to you

- the lease payment is clearly lower than expected bill savings

- the contract has fair transfer and buyout terms

- you understand how escalators work

- you are comfortable with third-party ownership

A solar lease may be weaker when:

- you want maximum long-term savings

- you want to claim ownership-based incentives

- you may sell your home soon

- the lease has high annual escalators

- the buyout terms are unclear

- you want full control over the system

Questions to Ask Before Choosing a Loan or Lease

Before signing a solar loan or lease, ask:

- Who owns the system?

- What is the cash price?

- What is the financed price?

- What is the APR?

- Are there dealer fees?

- What is the total repayment amount?

- What is the monthly payment?

- Does the payment increase over time?

- Who receives incentives?

- Who handles maintenance?

- What happens if the system underproduces?

- What happens if I sell my home?

- Can I buy out the contract?

- Can I prepay the loan?

- Are there liens, UCC filings, or transfer requirements?

- What happens if I need roof work?

Get the answers in writing. Do not rely only on verbal explanations.

Common Solar Loan vs Lease Mistakes

| Mistake | Why It Can Hurt You | Better Approach |

|---|---|---|

| Choosing based only on monthly payment | May hide higher total cost or weaker savings | Compare total cost, ROI, and contract length |

| Ignoring ownership | Ownership affects incentives, resale, and long-term value | Ask who owns the system |

| Not comparing cash and financed price | Dealer fees may be hidden | Ask for both prices |

| Ignoring lease escalators | Payments may rise and reduce savings | Review annual increases and total contract cost |

| Assuming you receive incentives | Lease customers may not receive ownership-based incentives | Ask who receives incentives |

| Forgetting home sale terms | Transfer or buyout issues can delay closing | Review sale, transfer, and buyout clauses |

| Trusting verbal promises | The written contract controls | Get every important claim in writing |

External Sources to Check

Before choosing a solar loan or lease, review official consumer guidance and verify contract terms.

- FTC consumer advice on solar power for your home

- CFPB consumer advisory on solar loans

- CFPB issue spotlight on solar financing

- Energy.gov homeowner guide to solar financing

- Your state consumer protection office or public utility commission for local solar consumer guidance

FAQ About Solar Loan vs Lease

Is a solar loan better than a solar lease?

A solar loan may be better if you want ownership, long-term savings potential, and possible access to ownership-based incentives. A lease may be better if you want lower upfront cost and less maintenance responsibility, but the contract terms must be reviewed carefully.

Do I own the solar panels with a loan?

Usually, yes. With a solar loan, the homeowner typically owns the system while repaying the loan. However, the loan terms matter, especially if the loan is secured or includes special filings or transfer rules.

Do I own the solar panels with a lease?

Usually, no. With a solar lease, the solar company or financing company typically owns the system. You pay a monthly amount under the lease contract.

Which has better ROI: solar loan or lease?

A solar loan often has stronger long-term ROI potential because the homeowner usually owns the system. However, a high-cost loan can reduce ROI. A lease may have lower upfront cost but usually limits ownership upside.

Can I claim solar incentives with a lease?

Usually, the system owner claims ownership-based incentives. In a typical lease, the homeowner does not own the system, so the homeowner should not assume they receive tax credits or ownership-based incentives.

What happens if I sell my home with a solar loan?

You may need to pay off the loan, transfer it, or handle it at closing depending on the loan agreement. Ask your lender and installer for the exact home sale process before signing.

What happens if I sell my home with a solar lease?

The buyer may need to assume the lease, qualify for transfer, or negotiate a buyout. Lease transfer terms can affect the sale process, so review the contract before signing.

Should I compare a solar loan and lease by monthly payment?

Monthly payment matters, but it is not enough. Compare ownership, total cost, incentives, escalators, maintenance, home sale terms, contract length, payback period, and long-term ROI.

Conclusion

The solar loan vs lease decision comes down to ownership, cost, contract terms, and long-term financial goals.

A solar loan may be better if you want to own the system, keep more long-term upside, and potentially qualify for ownership-based incentives. A solar lease may be better if you want lower upfront cost and less maintenance responsibility, but you usually give up ownership and some long-term savings potential.

Do not choose based only on monthly payment. Compare total cost, cash price, financed price, APR, lease escalators, incentive treatment, resale rules, maintenance terms, and payback period.

Before signing, run both scenarios with the MySolarROI solar ROI calculator. It can help you compare system cost, monthly savings, financing impact, payback period, and long-term ROI before you commit.