A solar loan calculator helps estimate how financing affects the real cost of going solar.

That matters because a solar quote with a low monthly payment can still have a high total repayment amount. Interest, dealer fees, loan term, financed price, and incentive assumptions can all change solar payback and ROI.

A good solar loan calculation should answer more than one question:

What will I pay each month, what will I pay in total, and how does the loan affect my solar savings?

This guide explains how to use a solar loan calculator, what inputs matter, how to compare cash price vs. financed price, how dealer fees affect the real cost, and how loan payments change monthly cash flow, payback period, and long-term ROI.

Before accepting a financed solar quote, use the MySolarROI solar ROI calculator to compare system cost, loan terms, annual savings, incentives, payback period, and long-term return.

What Is a Solar Loan Calculator?

A solar loan calculator estimates the financial impact of borrowing money to install solar panels.

It may estimate:

- monthly loan payment

- total interest paid

- total repayment amount

- cash price vs. financed price

- effect of dealer fees

- solar loan payback period

- monthly cash flow after bill savings

- long-term solar ROI

Solar loans can be useful because they allow homeowners to install solar without paying the full cost upfront. But they can also reduce savings if the loan has high interest, a long term, or financing-related price increases.

Energy.gov’s homeowner solar financing guide explains that residential solar financing options include cash purchases, loans, leases, and PPAs, each with different advantages and disadvantages. :contentReference[oaicite:2]{index=2}

Solar Loan Calculator: Inputs You Need

A useful solar loan calculator should ask for more than the monthly payment.

| Input | Why It Matters | Example |

|---|---|---|

| Cash price | Shows the base system cost without financing | $24,000 |

| Financed price | Shows whether financing increases the system cost | $28,000 |

| Down payment | Reduces amount financed | $0 or $2,000 |

| Loan amount | Principal used for payment calculation | $28,000 |

| APR | Shows annualized borrowing cost | 6.99% |

| Loan term | Determines how long payments last | 10, 15, 20, or 25 years |

| Dealer fee | May be built into financed price | Not always shown separately |

| Incentive paydown assumption | Some loans assume future incentive payment | Payment may change if not paid down |

| Estimated annual solar savings | Needed to calculate cash flow and payback | $1,800/year |

If an installer only shows a monthly payment and not the cash price, financed price, APR, loan term, and total repayment amount, the financing is not transparent enough.

Solar Loan Payment Formula

Most fixed-rate solar loans use a standard installment loan payment formula.

You do not need to calculate it by hand, but understanding the inputs helps you compare offers.

The core variables are:

- loan amount

- interest rate

- loan term

- payment frequency

In plain English:

Higher loan amount + higher APR + longer term = more total interest paid

A longer loan term may lower the monthly payment, but it can increase total repayment.

| Loan Term | Monthly Payment Effect | Total Interest Effect |

|---|---|---|

| Shorter term | Higher monthly payment | Usually less total interest |

| Longer term | Lower monthly payment | Usually more total interest |

| Lower APR | Lower payment and interest | Usually better if fees are not higher |

| Higher APR | Higher payment and interest | Can reduce ROI |

Do not compare loan offers by APR alone. A loan with a lower APR but a much higher financed price may not be the better deal.

Cash Price vs. Financed Price

One of the most important solar loan calculator inputs is the difference between cash price and financed price.

The cash price is the price if you pay without using the installer’s loan product.

The financed price is the price under the loan offer.

Sometimes the financed price is higher because the loan includes dealer fees, lender fees, or financing-related markups.

| Quote Item | Example A | Example B |

|---|---|---|

| Cash price | $24,000 | $24,000 |

| Financed price | $24,000 | $29,000 |

| APR | 8.99% | 3.99% |

| Why comparison is tricky | Higher APR but no price increase | Lower APR but higher financed price |

At first glance, Example B may look better because the APR is lower. But if the financed price is $5,000 higher, you need to compare total repayment, not just APR.

CFPB has warned consumers to watch for problems and pitfalls in solar energy loans, including confusion around payment terms, costs, and contract obligations. :contentReference[oaicite:3]{index=3}

Dealer Fees and Solar Loans

Dealer fees are one of the most confusing parts of solar financing.

A dealer fee is a financing-related cost that may be built into the price of the system. It can make the financed price higher than the cash price.

Dealer fees are not always shown clearly to homeowners.

Before accepting a solar loan, ask:

- Is there a dealer fee?

- How much is it?

- Is it included in the financed price?

- What is the cash price without the dealer fee?

- What is the total repayment amount?

- Would another loan option have a lower total cost?

| Financing Structure | What to Watch |

|---|---|

| Low APR with higher financed price | Dealer fee may be built into the system cost |

| Higher APR with lower system price | Monthly payment may be higher, but total cost could be competitive |

| No-fee loan | APR may be higher, but total repayment may be clearer |

| Installer-arranged financing | Convenient, but compare with outside financing options |

The best loan is not always the one with the lowest advertised APR. It is the one with the best total cost for your situation.

How Solar Loan Terms Affect Monthly Cash Flow

Solar savings and solar loan cash flow are not the same.

Bill savings estimate how much your electric bill may decrease.

Monthly cash flow compares bill savings with the solar loan payment.

Example:

| Monthly Item | Example |

|---|---|

| Estimated electric bill reduction | $150/month |

| Solar loan payment | $135/month |

| Estimated monthly cash flow | $15/month positive |

This example looks positive, but it may change if:

- the system produces less than expected

- utility export credits are lower than assumed

- fixed charges remain on the bill

- the loan payment increases later

- the incentive paydown is not made

- interest and fees are higher than expected

Ask the installer whether the monthly payment assumes you will apply an incentive or tax credit to the loan later. If you do not make that paydown, the payment may change depending on the loan terms.

Solar Loan vs. Solar Payback Period

Solar loan payment and solar payback period are related, but different.

Payback period estimates how long it may take for solar savings to recover your net system cost.

The basic formula is:

Solar payback period = net solar system cost ÷ annual electricity bill savings

Example:

| Input | Cash Scenario | Loan Scenario |

|---|---|---|

| System cost used in calculation | $24,000 | $29,000 financed price |

| Verified incentive | $1,000 | $1,000 |

| Net cost before interest | $23,000 | $28,000 |

| Estimated annual savings | $1,800 | $1,800 |

| Simple payback before interest | 12.8 years | 15.6 years |

Simple calculations:

$23,000 ÷ $1,800 = 12.8 years

$28,000 ÷ $1,800 = 15.6 years

This does not include all loan interest. It simply shows how a higher financed price can lengthen payback even before total interest is considered.

For more detail, read the solar payback period guide.

Mini Case Study: Comparing Two Solar Loans

Here is a simplified example. These numbers are for illustration only and are not guaranteed.

Actual results depend on system cost, APR, loan term, dealer fees, electricity rates, incentives, net metering, financing terms, tax situation, and actual production.

| Loan Detail | Loan A | Loan B |

|---|---|---|

| Cash price | $24,000 | $24,000 |

| Financed price | $24,000 | $29,000 |

| APR | 8.99% | 3.99% |

| Loan term | 15 years | 25 years |

| Estimated annual solar savings | $1,800 | $1,800 |

| Key concern | Higher APR | Higher financed price and longer term |

Loan B may show a lower monthly payment because the APR is lower and the term is longer. But that does not automatically make it cheaper.

To compare both loans fairly, calculate:

- monthly payment

- total repayment amount

- total interest

- difference between cash and financed price

- monthly cash flow after solar bill savings

- payback period

- long-term ROI

Run both options through the MySolarROI calculator before signing. Use the same production, electricity rate, incentive, and export credit assumptions for each loan.

How Incentives Affect Solar Loan Calculations

Incentives can reduce net system cost if you qualify, but they can also complicate loan calculations.

Some solar loans assume that you will apply an incentive or tax credit to the loan after receiving it. If you do not make that paydown, your monthly payment may increase or your loan may re-amortize depending on the contract.

Ask:

- Does this loan assume an incentive paydown?

- When is the paydown due?

- What happens if I do not receive the incentive?

- What happens if I receive less than expected?

- Will my monthly payment increase?

- Is the incentive guaranteed or estimated?

For new 2026 residential solar installations, be careful with federal tax credit assumptions. Do not automatically assume the old 30% federal residential credit applies. Read the federal solar tax credit 2026 guide and the solar tax credit calculator guide.

Solar Loan vs. Cash Purchase

A cash purchase is usually simpler because there is no loan interest or dealer fee. A solar loan may be more practical if you want to preserve cash or avoid paying the full cost upfront.

| Factor | Cash Purchase | Solar Loan |

|---|---|---|

| Upfront cost | Highest | Lower upfront cost |

| Interest | None | Depends on APR and term |

| Dealer fees | Usually not applicable | May be included in financed price |

| Monthly payment | No loan payment | Required loan payment |

| ROI potential | Often strongest | Can still be strong with fair terms |

| Cash flexibility | Uses more cash upfront | Preserves more cash |

If you can pay cash without financial stress, cash may provide stronger long-term ROI. If cash is not practical, a transparent loan may still work if the terms are fair.

For a broader comparison, read the solar financing comparison guide.

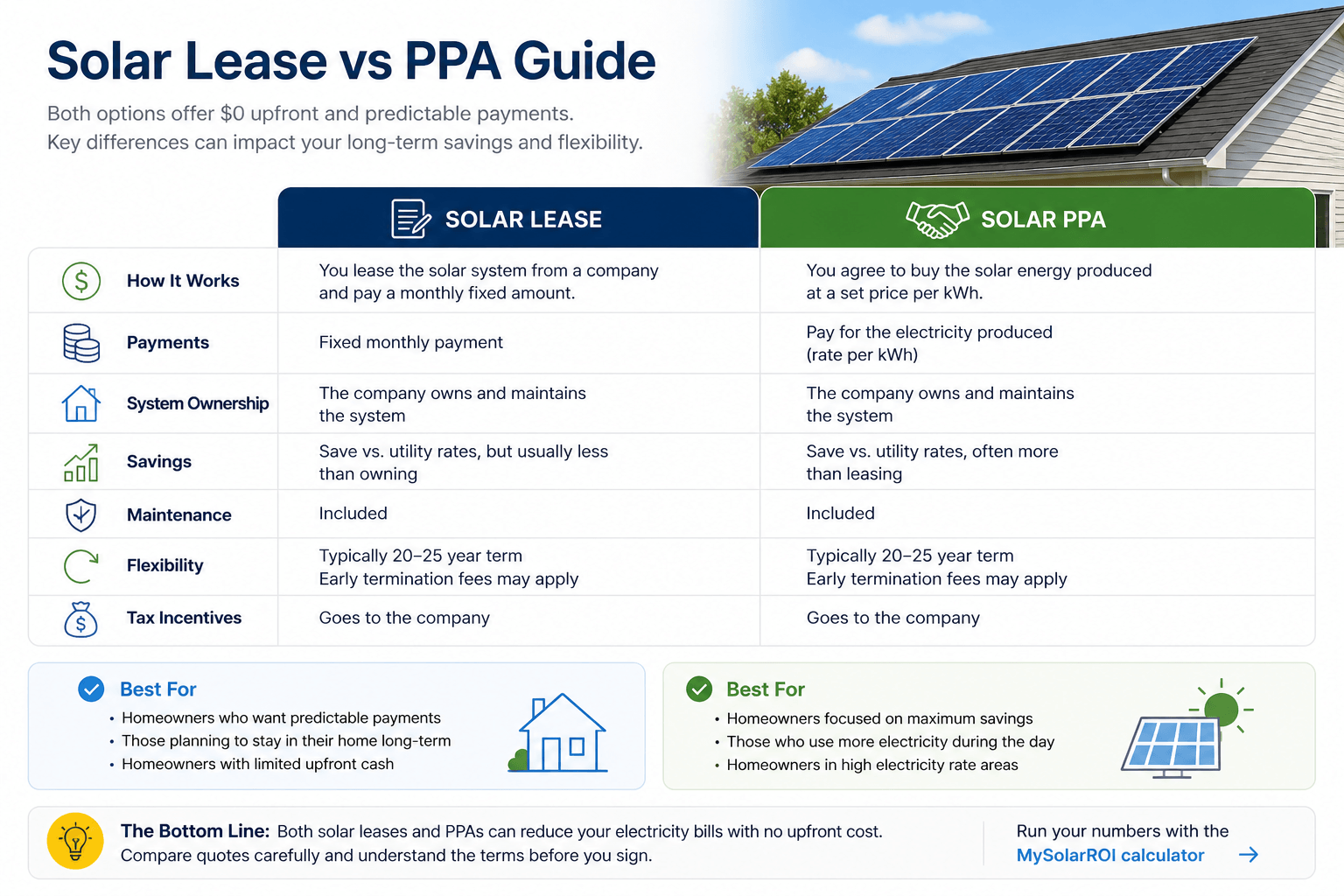

Solar Loan vs. Lease or PPA

A solar loan usually means you own the system while repaying the lender. A lease or PPA usually means a solar company or financing company owns the system.

| Question | Solar Loan | Lease or PPA |

|---|---|---|

| Who usually owns the system? | Homeowner | Solar company or financing company |

| Who may receive ownership-based incentives? | Homeowner may qualify if eligible | System owner may receive them |

| Payment type | Loan payment | Lease payment or PPA energy rate |

| Long-term upside | Can be stronger after loan payoff | Usually limited by contract terms |

| Home sale | Loan payoff or transfer may matter | Contract transfer or buyout may matter |

FTC notes that homeowners can buy a system, lease a system, or sign an agreement to buy solar power, and should understand what they are getting before agreeing to anything. :contentReference[oaicite:4]{index=4}

For a direct comparison, read the solar loan vs lease guide.

Questions to Ask Before Accepting a Solar Loan

Before signing a solar loan, ask:

- What is the cash price?

- What is the financed price?

- What is the APR?

- What is the loan term?

- What is the monthly payment?

- What is the total repayment amount?

- Is there a dealer fee?

- Is the dealer fee included in the financed price?

- Does the loan assume an incentive paydown?

- What happens if I do not receive the incentive?

- Can I prepay the loan?

- Are there prepayment penalties?

- Is the loan secured or unsecured?

- Will there be a lien, UCC filing, or other notice?

- What happens if I sell my home?

- What happens if the system underproduces?

Get the answers in writing. The written loan agreement matters more than verbal explanations.

Common Solar Loan Calculator Mistakes

| Mistake | Why It Can Mislead You | Better Approach |

|---|---|---|

| Comparing only monthly payment | Can hide high total repayment | Compare total repayment and ROI |

| Ignoring cash price | You may miss financing markups | Ask for cash and financed prices |

| Comparing APR without dealer fees | Low APR may come with higher financed price | Compare total cost, not APR alone |

| Ignoring loan term | Longer terms may increase total interest | Compare multiple term lengths |

| Assuming incentives are guaranteed | Payment may change if incentive is not received | Use verified incentives only |

| Ignoring utility savings assumptions | Loan may look affordable if savings are overstated | Check rates, production, and net metering rules |

| Not checking home sale terms | Loan payoff or transfer can matter later | Ask what happens if you sell |

How to Use a Solar Loan Calculator Safely

Use this process:

- Enter the cash price.

- Enter the financed price separately.

- Enter the loan amount.

- Enter APR and loan term.

- Calculate monthly payment.

- Calculate total repayment.

- Compare total repayment with cash price.

- Add estimated annual solar bill savings.

- Compare monthly payment with monthly savings.

- Estimate payback period and ROI.

- Run conservative, base-case, and optimistic scenarios.

Do not use a calculator to justify a loan you do not understand. Use it to uncover the true cost and compare options.

External Sources to Check

Before accepting a solar loan, review official consumer guidance and verify contract terms.

- CFPB consumer advisory on solar loans

- CFPB issue spotlight on solar financing

- FTC consumer advice on solar power for your home

- Energy.gov homeowner solar financing guide

- Your lender’s loan agreement and payment schedule

- Your state consumer protection office or attorney general’s office

FAQ About Solar Loan Calculators

What does a solar loan calculator do?

A solar loan calculator estimates monthly payment, interest, total repayment, and how financing affects solar savings, payback period, and ROI. It should include cash price, financed price, APR, loan term, and incentives.

What is the most important solar loan number?

Monthly payment matters, but total repayment is usually more important for ROI. Also compare cash price, financed price, APR, dealer fees, loan term, and whether incentives are assumed.

Can a low APR solar loan still be expensive?

Yes. A low APR loan can still be expensive if the financed price is much higher than the cash price because of dealer fees or financing-related markups.

What is a solar dealer fee?

A dealer fee is a financing-related cost that may be built into the system’s financed price. It can make the financed price higher than the cash price, even when the advertised APR looks low.

Should I compare solar loan payment to my electric bill?

Yes, but carefully. Compare estimated bill savings with loan payment, fixed utility charges, export credit assumptions, and production estimates. Monthly cash flow is not the same as total ROI.

Does a solar loan affect payback period?

Yes. Loan interest, dealer fees, and a higher financed price can lengthen payback period and reduce ROI compared with a cash purchase.

Should I use incentives in a solar loan calculator?

Only include incentives you reasonably expect to qualify for. If the loan assumes an incentive paydown, ask what happens if you do not receive the incentive or receive less than expected.

Is a solar loan better than a lease?

A solar loan may be better if you want ownership and long-term upside. A lease may have lower upfront cost and maintenance support, but you usually do not own the system. Compare contract terms, incentives, resale impact, and ROI.

Conclusion

A solar loan calculator is useful only if it shows the real financing picture.

Do not rely only on monthly payment. Compare cash price, financed price, APR, loan term, dealer fees, total repayment, incentive assumptions, monthly cash flow, payback period, and long-term ROI.

A solar loan can make sense when the system price is fair, the financing is transparent, and the expected savings support the payment. A solar loan can weaken ROI when fees, interest, or inflated financed prices reduce long-term savings.

Before signing, use the MySolarROI solar ROI calculator to compare your solar loan against cash, savings, incentives, and payback assumptions.